Bailiff's Account 1545

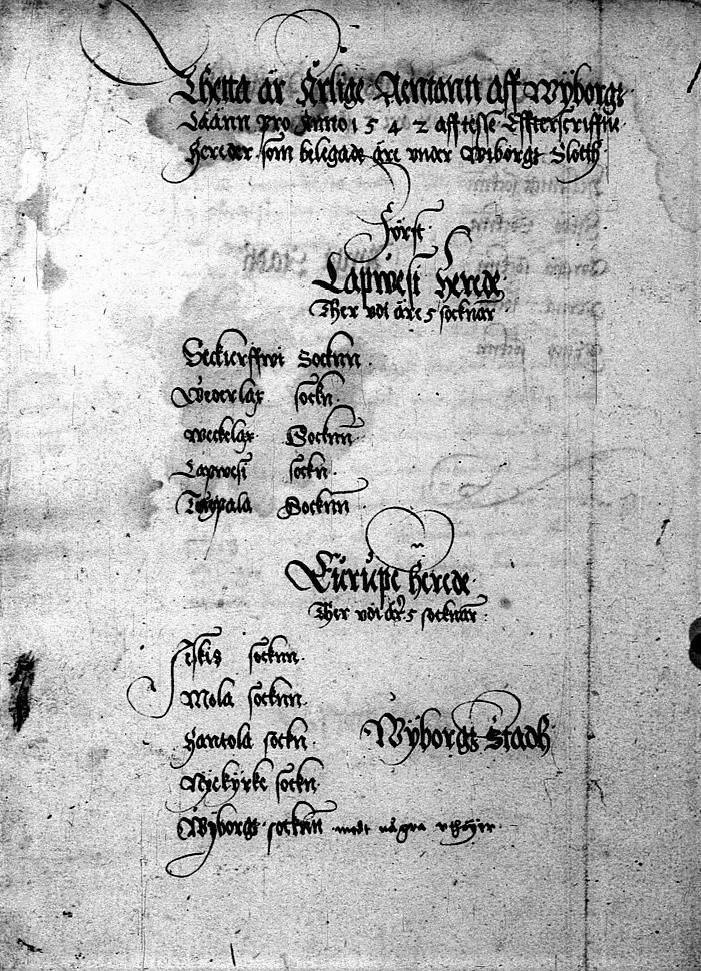

Bailiwicks of Karelia, accounts of Vyborg province, 1542.

Finnish National Archives, http://digi.narc.fi/digi/view.ka?kuid=2659673.

When Sweden left the Kalmar Union in 1521, King Gustav reformed local government. As in the Middle Ages (in the Nordic countries, the period from c. 1200–1500), castles were the centres of local administration. In the medieval period, the king's most trusted men were often castellans, and the territories administered from the castle were often in their fiefs. In Gustav Vasa's reform, the crown tax administration was separated from other royal tasks. Other royal affairs (such as correspondence and diplomacy) were handled by the chancellery and financial and tax affairs by the chamber (camera in Latin). Castellans began to be paid, becoming, as it were, officials. Castellans were assisted in tax affairs by the castle bailiffs and their scribes. Castle administration was divided into basic units of local administration, or bailiwicks (voutikunta). The royal bailiff took care of their administration and tax collection. The collected taxes and tax bases now required written explanations on the German model. The bailiffs' and castle administrative accounts were to be sent to the royal chamber in Stockholm to be checked. Thus the first series of running account books describing crown taxation, called the bailiffs' accounts, was born. The bailiffs' accounts from Finnish territory have generally been preserved from the end of the 1530s to the provincial administration reform of 1634. The bailiffs' accounts are an important source for sixteenth-century economic history, settlement and population history and social history.

The bailiffs' accounts are organized chronologically by castle administration in the National Archives of Finland. In addition, there is the series of general documents, which includes documents that do not belong to one bailiff or castle administration accounts. These include toll accounts and hospital (institutions for the care of the poor and sick) accounts and some fragments of early district court records. The bailiffs' accounts first report on area from which the accounts are drawn up, the bases of parish taxation, which varied in different parts of the kingdom and even within one castle's administrative territory. Then the calculated collected tax is reported by type of goods, the reductions made from the taxes and the real bailiwick tax income for crown use. The bailiffs' accounts then describe the use of the tax goods, that is, where they are taken to (for example, for the needs of castles) and other payments made from taxation. The bailiffs' accounts close with the income and expense receipts on which the book–keeping was based. The most important of these is the land register, which carefully lists the bases of taxation for households paying taxes. Other significant receipts for the bailiffs' accounts include the tithe lists, fine lists, livestock and sowing lists and fief letters.